Remote Seller Nexus Chart

This remote seller nexus chart lists the states that have passed one or more types of legislation regarding nexus.

If you’ve been following sales tax developments lately – or have been keeping up with our blog, Twitter, LinkedIn group, or News and Tips – you’re undoubtedly aware of the South Dakota v. Wayfair court case that has been dominating news cycles lately.

This seminal court case was just gaining momentum in January. In the short time since then, so much has happened in the world of remote seller nexus.

Most significantly, the U.S. Supreme Court heard oral arguments on South Dakota v. Wayfair on April 17, for which I traveled to Washington, D.C. to see first-hand! It was amazing to be a part of that historic moment at the nation’s capital.

Now that we’ve had time to digest and analyze the oral arguments, we can explore the technical aspects and expound on what this may all mean for the future of sales tax.

I asked 5 experts to weigh-in on what happened and what it means. We spoke to experts that all have a different perspective in sales tax in order to provide you a well-rounded analysis from industry, to legal minds, to a tax commissioner.

Each one of the experts we spoke to were in D.C. for the momentous event and bring different perspectives to the case. I spent time talking to each of them and I’ll be incorporating their comments into my analysis below as well as sharing my thoughts.

Many thanks to our experts willing to share their interpretations of the events with Sales Tax Institute readers:

Barb and Stephen were in the courtroom while Jordan and Marilyn were able to hear the arguments from the lawyer’s lounge at the Supreme Court. Adam and I only were able to hear 3 minutes of the arguments but had the bonding experience of waiting in line for over 5 hours!

Jordan, Marilyn, and Barb have all made a return visit to the Supreme Court for a tax case. Steve had gone before as a tourist, but this was his first tax case. Seeing the Supreme Court in action has been on Adam’s bucket list. Me – I had to be there as I wanted to be part of history being made. And I definitely want to go back to hear a full argument.

Before we get into the analysis, I asked everyone for their predictions going into the arguments – what did they think would happen before the arguments took place? All of them pointed to the fact that four justices had to agree to take the case. So that would give some thought that there might be four in favor of South Dakota. But, it is important not to read too much into this – as some of those might have wanted to simply stop the questions of whether they will take a case.

Advance predictions were fairly consistent – almost everyone felt that the decision would be a win by South Dakota – from a leaning towards a win to a 90% chance of a win by South Dakota.

Adam thought it was a “slam dunk” overturn of Quill. Even Barb, as a tax professional of an industrial manufacturer, providing the taxpayer perspective, thought Quill’s time was over.

I thought the Court wouldn’t have taken the case unless they wanted to make a change. Jordan disagreed. His thought was that this is a commerce clause issue which would require a law change. That isn’t something the Supreme Court can do as they are not legislators. He felt that the Court would either remand the case back for development of the facts or they would rule similarly as they did in Quill with a direction to Congress to fix the problem. We’ll revisit predictions later after we talk about what happened.

The justices didn’t waste any time jumping in to ask questions. Justice Sonia Sotomayer asked the first question after South Dakota Attorney Jackley only got out 2 sentences.

Her question, and one of the focus points from the justices, was that the real problem isn’t the Quill decision but rather the fact that the states don’t have a mechanism to collect the tax directly from the consumers. This question, although pointed, helps to set the stage that this isn’t a new tax that South Dakota is imposing.

What the South Dakota provision addresses is when can the state require a remote seller to collect the tax on sales made to customers in their state. This is really the challenge faced by the states. And it is important to remember – this isn’t a new tax. Every state with a sales tax has a complimentary use tax. Customers, particularly individuals rather than businesses, have a very low compliance rate of paying the use tax.

For a number of years, most of the states that impose both a sales tax and an individual income tax have included either a line on the individual income tax return or information in the instructions to encourage individuals to remit any use tax due. However, the compliance rates are still very low. This is what has prompted the states to impose the various types of remote seller legislation.

What South Dakota enacted is referred to as Economic Nexus since it doesn’t require any physical presence whatsoever – just sales above a specified threshold. In South Dakota’s case, the threshold is 200 transactions OR $100,000 in sales. There are 16 states (including Indiana where Adam Krupp is Commissioner) that have enacted some sort of economic nexus.

Technically, none of these states can enforce their provisions until we hear from the Supreme Court on South Dakota v. Wayfair but that hasn’t stopped some from trying. The reason is that in the Quill case, which the Supreme Court decided in 1992, they decided that substantial physical presence is the test under the dormant commerce clause that would determine whether a state could require a remote seller to collect sales tax. This has been the standard since then.

What South Dakota is really asking the Court to do is to overturn their own decision in Quill. This is a big ask. Why? There is a concept referred to as “stare decisis” which literally translates as “to stand by decided matters”. The phrase “stare decisis” is itself an abbreviation of the Latin phrase “stare decisis et non quieta movere” which translates as “to stand by decisions and not to disturb settled matters”. This gives stability to the rule of law so that everyone can set up their operations to comply. A case can be decided differently – overruling the prior decision – when there is a change in law or a change in facts. In this case, there hasn’t been a change in law. So the question is whether there has been a change in the facts since Quill was decided that would warrant the Supreme Court overturning its prior decision. This is really the overriding concern as the justices asked their questions of both sides.

Now that we have set the stage for the technical question, let’s get back to the oral arguments. Something that everyone I talked to agreed on was that this decision might not be as much a legal decision as it will be a public policy decision. I believe this is what was underlying some of the frustration that everyone sensed from the justices at the oral arguments, as this isn’t something they are comfortable doing. Their role is to interpret the law, not make the law. And this is a big part of the argument by Wayfair – let Congress make the law. We heard a number of the justices ask this exact question.

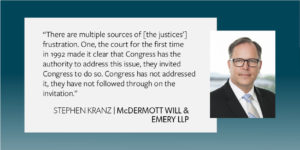

South Dakota, as well the U.S. Solicitor General who also argued on behalf of South Dakota, made the point that the Supreme Court asked Congress to deal with this issue 26 years ago in the Quill decision and they still haven’t acted, or have they? That is what some people are arguing – Congress’ lack of action is really their action. So if the Court follows stare decisis and upholds Quill and includes a direction to Congress to address the issue – do you think they will actually do anything?

The person I talked to that is closest to what is happening in Congress on this is Steve – so I asked him if he thinks Congress would act. He doesn’t feel optimistic about that. “Congress has been ready to act since 1973” according to Steve, and they haven’t. Proposals have been pending and only once has the Senate passed anything. House Judiciary Chairman Goodlatte has single handedly held up any action in recent years. He did hold a hearing a few years ago at which Steve testified. But, nothing happened in the House. Interestingly, Rep. Goodlatte was one of four congress members in the courtroom. Maybe hearing it firsthand will give them some perspective.

Moving on to the crux of the case. There were really 3 main points that were focused on in the questions – threshold, retroactivity, and cost/burden. Let’s dig into each one and understand the points and get perspectives from our experts.

The South Dakota law sets the economic nexus threshold at $100,000 in sales or 200 separate transactions in a year to customers in the state.

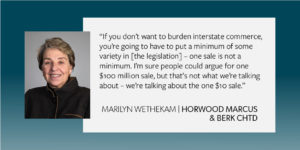

Early on in the questioning, Justice Sotomayor raised the question – “What’s the contact that you have to do to impose this obligation? How much contact is enough to justify placing this obligation on an out-of-town seller?” AG Jackley responded that we should look to Complete Auto and the four-prong test to make that decision. He also responded that economics should be considered – which makes sense given the South Dakota law. But what was totally unexpected to me as well as to all our experts was the next response from AG Jackely to the question as to what is the minimum everywhere else? His response – “The minimum would be one sale because, if you look at Complete Auto, that creates the nexus.” The Solicitor General reiterated this exact point during his period of questioning.

So, what do our experts think is the right threshold?

Marilyn’s point was that one sale doesn’t meet the threshold of substantial nexus. One is isolated and isn’t an economic exploitation of the market. I posed the question as to whether the threshold in any state should be an AND test rather than an OR test with the dollars and number of transactions. This came up in some of the questions – that the average B2C transaction can be very low ($10-$12) so even at 200 transactions this is way below the $100,000 sales threshold. This raises the question: should it be a higher number of transactions since the real concern of the states is the B2C market over the B2B transactions?

Steve was disappointed that South Dakota didn’t stay on the message of their threshold. After all, this case is about the South Dakota law which does have a threshold that is much higher than one sale.

Adam had the same point – he thought they should have focused on the threshold that was being litigated. Although he supported the one sale concept, he still had some concerns about this minimal level. “What if the transaction was erroneous? What if the seller didn’t know the transaction happened? What if the sale was returned?” These all could be problematic if registration is required after one transaction. Keep in mind that the Indiana threshold matches the South Dakota threshold which Adam supports is an appropriate threshold.

Jordan brought up a good point about the difference between the due process and commerce clause. Due Process is a minimum connection, and this could be as little as one sale. So, if the justices overturn Quill, then commerce clause isn’t really the relevant test – due process is. So that would support a threshold of one sale. And that would say that 200 transactions certainly meet the due process threshold. That is a scary thought isn’t it?

Barb, from a taxpayer’s perspective, gave an interesting alternative option. Maybe it should be a percentage of sales rather than a number of transactions or even a flat dollar amount. This could help smaller businesses – but it would also disadvantage small population states – like South Dakota.

And what do I think? Definitely not one sale! I asked the question about an AND threshold test as I do think that would make more sense and help businesses that have low dollar sales which usually also mean less profit to absorb the cost of collection. A few of the states use a $500,000 threshold and to me that seems a bit more reasonable. Maybe even without a transaction count. This would act as a small business protection. The proposed federal legislation doesn’t have a per state small business threshold but a total remote sales threshold. That is troubling to me as in today’s rules there are too many different tests to determine if you are a remote seller. So, I think what would be fair is a higher dollar threshold per state where physical presence isn’t established with either sales volume AND transaction counts or a much higher transaction threshold.

We all know this is really driving the taxpayer frustration – particularly small businesses. What does it cost to collect sales tax? This is a fact that really would have been best to have flushed out in the case. But, due to the process followed in getting the case to the Supreme Court as quickly as it did (using summary judgement), there wasn’t really any meat to the case. Justice Stephen Breyer actually asked if anyone knows how much it costs Amazon to voluntarily comply. No one did – and this wasn’t addressed in any briefs as Amazon isn’t a party to the case. But what does it cost? Different briefs argued different amounts ranging from $12 to $250,000. Now that is a wide margin!

Unfortunately, there hasn’t been a recent comprehensive independent study on this point. I’ve spent significant energy looking at this as I wrote an article that was published in State Tax Notes on how things have changed since the Quill decision to today in the sales tax technology field. There are costs to comply – no argument from me on that. But, a point I make in the article and that I raise to people that say there should be no cost or burden, is that complying with laws is part of the regular costs of being in business. An article was published by an e-commerce CEO recently discussing the costs of collection that was cited in one of the respondent’s briefs for the case. He brings up valid points but his research isn’t comprehensive about the costs all e-commerce retailers might see. I agree more work needs to be done to reduce efforts and costs of collection and states needs to simplify some of their rules. The sales tax software companies can also look for ways to facilitate the integration and most importantly the product mapping exercise.

I am a small business owner and I make business decisions about what I will do taking into consideration the costs and that includes costs to comply with all types of laws. That can be whether to launch a new product that might require sales tax collection to hiring an employee that lives in another state which would require payroll compliance and income tax filing in a new state.

I do, however, think the burden needs to be reasonable. And that goes back to what is the right threshold level. A threshold of one transaction, as suggested by AG Jackely, makes this burden unreasonable. But sales of at least $100,000 (or higher as discussed above) into a state makes it more reasonable.

Something else to keep in mind is there is a base cost to collect tax in one state. Adding more states is not a duplicative cost but incremental.

It was in this line of questioning that we heard from Justice Neil Gorsuch who raised the question as a comparative cost to the notice and reporting rules such as the Colorado rule. He sat on the appellate bench that decided the Direct Marketing Association case. His point was that the real difference isn’t between collecting and not collecting but between collecting sales tax and complying with notice and reporting rules. I agree on this point. If the Court rules in favor of Wayfair, this is where I see the states moving and quickly. We’ve already seen 2 states pass this type of expanded requirement this year. Justice Gorsuch believes the notice and reporting regimes are more burdensome (and so do I). But Mr. Isaacson, representing Wayfair, believes sales tax collection is more burdensome.

What do our other experts think about cost and burden?

Let’s start with the taxpayer’s perspective from Barb.

She believes that collecting tax could be a more significant burden on small companies but believes large taxpayers should be required to collect. It is a cost of being in business – so on this point we agreed. She did point out that software can do part of the process, but there is more involved. I think we all agree on this. Product mapping is one of the biggest challenges companies face. Streamlined Sales Tax has helped in the participating states on some types of products but this needs to be expanded. Having worked with many clients on product mapping, it can be challenging. (Side note – check out our upcoming webinar where we’ll talk about this!)

What about the notice and reporting requirements? Barb’s point is that the biggest issue probably isn’t the cost or effort in complying. What is really at stake here is company reputation. How many companies really want to be turning in their customers to the state? Look at what happened in Connecticut. Newegg decided to turn over their customer list so the state could collect from the customers. Newegg ended up with egg on their face and very quickly decided to collect instead. In today’s social media world, I don’t know of a company that doesn’t need to think about the ill will that could be generated by a customer that didn’t like getting a notice from the state. And let’s face it, how many individuals really want to have to file another tax return? Let’s even look around at those of us that know we should be filing the use tax. Do you comply? I’ll admit I’m a rule follower so you can guess my answer.

What is the tax commissioner’s point of view? As you might guess, Adam thinks the sellers should collect. He believes that the voids in the market for appropriate technology will be met. Look at what has happened since Quill – there were two providers in 1992. Today there are many more with options for how to comply. The market has exploded and there is room for additional providers. Adam believes that if Quill is upheld, the states will continue to be creative. We already have cookie nexus – I’m sure they will come up with new and different approaches. He also raised the possibility of states using third parties to assist them regarding use tax collection by identifying purchases through access to financial data, for example. There are companies that claim to have the ability to use big data and a software algorithm to identify transactions where use tax is owed. States could then match the data to what has been reported on individual returns. This is aligned with Justice Sotomayor’s line of questioning during the Wayfair argument. He indicated that Indiana doesn’t plan on using a third party to assist in the collection and remittance of the tax. But that doesn’t mean other states might not go down this path. That scares me – think about what we’ve had to deal with on third party and contingent fee auditors for local home rule authorities and unclaimed property. I don’t think any taxpayer would look forward to that experience!

Our three attorneys think sellers would rather collect than comply with the notice and reporting. Steve, Jordan, and I all have clients that have opted to register and collect rather than face the notice and reporting rules. Marilyn believes the states need to make the registration process easier and I agree. Having just gone through a number of registrations for clients under the Multistate Tax Commission (MTC) Online Seller Registration program – that process is a challenge. No state is the same, and they ask questions that don’t always seem relevant. And the states have to stop requiring full social security numbers of officers.

Consistency on exemption documentation is another area that the states should consider. Do they really all need their own forms for something like resale? And why do they need a different form for all the different types of exemptions like in New York? That just adds unnecessary burden. Train the auditors what to look for on a standard form.

Another point Marilyn brought up is the vendor discount or seller compensation. This has been a sticking point in Streamlined as well as in the federal legislation. Some states offer a decent amount like Illinois at 1.75% of tax collected. Others like Florida offer a minimal amount – $30 per return. But a number of states don’t offer anything at all. Sellers are doing a service for the states and should be compensated at a reasonable amount.

Another point to think about that wasn’t addressed at all in the case is the impact on international sellers. Would the states require foreign sellers to comply? This is definitely the trend globally. Many countries now require remote sellers without any presence in the country to collect tax – particularly on digital goods and services sold to individuals. Some countries have thresholds, but others don’t. We are arguing about collecting tax across state lines but many of these same companies have a requirement to collect tax in a number of other countries with many more challenges like currency and language requirements.

So, the consensus from our group seems to be there are burdens; but being in business carries an obligation to comply with laws. Government has to do its part to make these burdens reasonable. After all, if the costs and burdens are too high, the businesses won’t survive – particularly small businesses. And small business is what drives our economy. According to the U.S. Census Bureau in 2017, small businesses make up: 99.9% of U.S. employer firms, 47.8% of private-sector employment, and created 1.4 million net jobs in 2014. We can’t afford to kill any significant portion of small business.

A major concern of everyone is what impact an overturn of Quill would have on periods prior to the date of the decision. South Dakota’s law specifically addresses this (as does Indiana) and limits the application to prospective periods. A number of the states that have already passed economic nexus laws did the same thing. But not all states agree.

A point addressed in the oral arguments was that 38 states signed on to a brief indicating that they would not enforce any change retroactively.

What does our group think?

Most would like to think the states that signed on to this would honor their position. But we all know what happens in bad economies and there is nothing binding the states to this position in the brief.

Marilyn doesn’t think the states will pursue retroactive collection. Steve doesn’t think the states will be “hogs” (remember they get slaughtered) and in this case it would be litigation. Even Adam doesn’t think retroactive application is fair and he thinks this is an area where Congress may need to step in. Barb’s point was that the person that made the agreement might not be here tomorrow, and who knows what condition the state will be in?

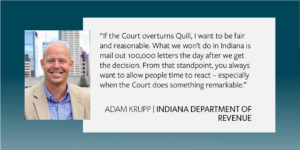

If South Dakota prevails, a big question is how quickly it will become effective. We can hope the two sides will come to an agreement similar to what happened in Colorado after the Direct Marketing Association case. Adam believes that is what the states should do – come up with a reasonable effective date and not just the day after the decision. That is his approach for Indiana.

Of course, all of this really just applies to pure economic nexus. If there is any physical presence such as inventory in the state for Amazon FBA (Fulfillment by Amazon) sellers, we all have examples of states that are going after these sellers aggressively. California is at the top of the list. I was a big supporter of the MTC Online Seller program and we helped a number of clients come into compliance through this program. Indiana wasn’t part of this but I worked with Adam and his staff and they agreed to a limited look-back (pay 2017 to current for both sales tax and income tax). In fact, they just announced this program is open to any online seller through the end of 2018. Thanks to Adam for being reasonable on this. If we can now just get some of his fellow Commissioners to join him (hint, hint)!

OK – that was a lot to cover!

What did our group find surprising and not surprising? Everyone was surprised that Justice Sotomayor asked the first question and was as pointed as she was. We all were also surprised that Justices Anthony Kennedy and Gorsuch were as quiet as they were. They have been the most vocal (Kennedy) or experienced (Gorsuch) on these issues. Maybe they wanted to give their peers more time to learn about what they were confused about. Many were surprised this was really a policy discussion and not as much legal discussion. And, as I’ve mentioned a few times, the focus wasn’t on the South Dakota law much at all.

What didn’t surprise anyone – Justice Clarence Thomas’s lack of questioning. This is typical for Justice Thomas. Jordan wasn’t surprised about the Court’s concern about retroactivity. Steve wasn’t surprised by Justice Gorsuch’s view of the Colorado regime and how he phrased his question about burden.

So, after the arguments, did the experts’ predictions change? Did yours?

Mine did and so did all of our group. Marilyn still thinks it’s a South Dakota win but closer – likely a 5-4 decision. Steve is in the same camp – close to 50/50 for South Dakota. He thinks Kennedy, Gorsuch and Thomas will vote to overturn Quill while Sotomayor and Kagan will not.

Jordan doesn’t think there are five justices that will uphold Quill. He doesn’t think they will give a half answer. He thinks there are three options – overturn Quill and uphold the South Dakota threshold; Uphold Quill and keep substantial physical presence; or remand the case to build the facts. But he thinks down deep they want Congress to act.

Adam doesn’t think it is as clear cut as he was expecting. He actually sees it as 5-4 and maybe to uphold Quill. He thinks Justice Breyer will be the deciding vote. His only real prediction is that it is much closer than it was before April 17.

Barb feels it would be hard for the justices to overturn Quill and set policy. She thinks they will send it to Congress to fix but in their decision will provide guidance on what they think the model should be.

And what do I think? I think it is also close but am going to hold that they wouldn’t have taken the case if they weren’t going to make a change. I’m thinking they will overturn Quill and affirm the South Dakota threshold. I don’t think they believe the threshold is one sale.

Now we are in the waiting phase. The Court indicated they would issue their decision by the end of June. Decisions are typically issued on Monday during May and June. So, the latest we should hear is June 25.

Might we hear earlier? Jordan thinks that could happen if they remand to the South Dakota Supreme Court. We will keep everyone posted and you’ll definitely hear from us as soon as a decision is rendered. Who knows? Maybe I’ll venture to D.C. again to try to be in the courtroom when they announce the decision.

In the meantime, we are keeping up on what the states are doing. The trend of states introducing and enacting remote seller nexus legislation has continued unabated in the first part of 2018. So far this year, 5 states have signed remote seller nexus legislation into law:

Nine states have introduced remote seller nexus legislation so far in 2018: Connecticut, Hawaii, Illinois, Iowa, Nebraska, New Mexico, New York, Oklahoma and Vermont. Whether these bills are enacted remains to be seen, but we’ll keep you updated (Pro tip: bookmark our Remote Seller Nexus Chart to stay up-to-date with the latest developments).

What is your prediction? What didn’t get addressed that you would have liked to hear more about in the oral arguments? Drop me a line and share your thoughts.

And if you want to read or listen to the arguments – here you go!

About the Author:

About the Author:Diane L. Yetter is a strategist, advisor, speaker, and author in the field of sales and use tax. She is president and founder of YETTER Tax and founder of the Sales Tax Institute. You can find Diane on LinkedIn and Twitter.